Federal Reserve Economic Data

Notes

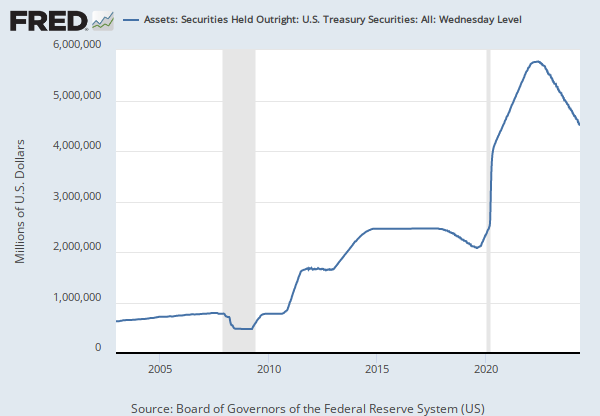

Source: Board of Governors of the Federal Reserve System (US)

Release: H.4.1 Factors Affecting Reserve Balances

Units:

Frequency:

Notes:

Reverse repurchase agreements are transactions in which securities are sold to primary dealers or foreign central banks under an agreement to buy them back from the same party on a specified date at the same price plus interest. Reverse repurchase agreements absorb reserve balances from the banking system for the length of the agreement. They are typically collateralized using Treasury bills. As with repurchase agreements, the naming convention used here reflects the transaction from the dealers' perspective; the Federal Reserve receives cash in a reverse repurchase agreement and provides collateral to the dealers.

Suggested Citation:

Board of Governors of the Federal Reserve System (US), Liabilities and Capital: Liabilities: Reverse Repurchase Agreements: Maturing in 16 Days to 90 Days: Wednesday Level [RREP1690], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/RREP1690, .

Release Tables

H.4.1 Factors Affecting Reserve Balances

Related Data and Content

Data Suggestions Based On Your Search

Content Suggestions