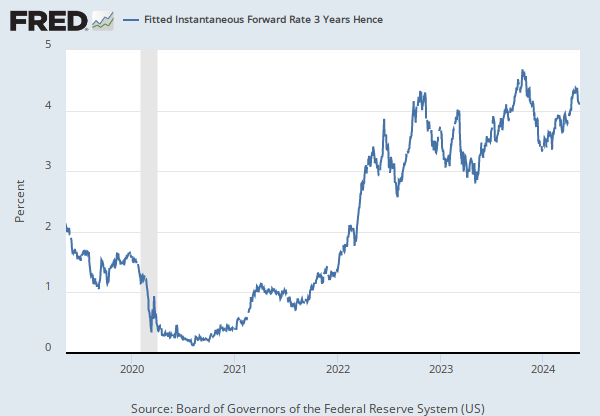

Observations

2025-03-28: 5.0383 | Percent, Not Seasonally Adjusted | Daily

Updated: Apr 1, 2025 2:03 PM CDT

Next Release Date: Not Available

Observations

2025-03-28:

5.0383

Updated:

Apr 1, 2025

2:03 PM CDT

Next Release Date:

Not Available

| 2025-03-28: | 5.0383 | |

| 2025-03-27: | 5.1054 | |

| 2025-03-26: | 5.0753 | |

| 2025-03-25: | 5.0497 | |

| 2025-03-24: | 5.0517 | |

| View All | ||

Units:

Percent,

Not Seasonally Adjusted

Frequency:

Daily

Fullscreen