Federal Reserve Economic Data

Notes

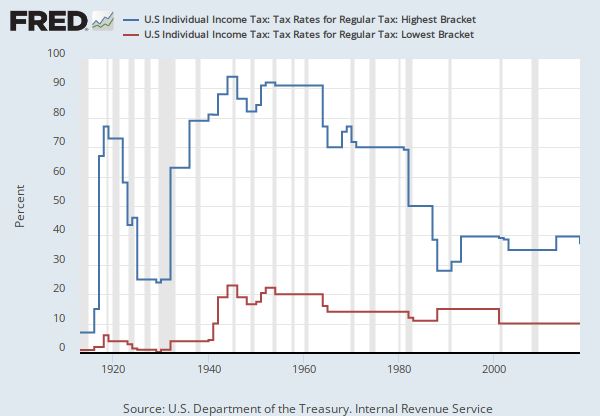

Source: U.S. Department of the Treasury. Internal Revenue Service

Release: SOI Tax Stats - Historical Data Tables

Units:

Frequency:

Notes:

Years represent the tax years .Starting with 1985, tax bracket boundaries were indexed for inflation, using the U.S. Department of Labor Consumer Price Index for Urban Consumers (CPS-U).

As stated by the source, tax rates shown are for the regular income tax, i.e., for normal tax and surtax, applicable to U.S. citizens and residents. Therefore, the rates exclude provisions unique to nonresident aliens. Tax rates exclude the effect of tax credits (which reduce the tax liability), except as noted, and several specific add-on or other taxes applicable to all or some tax years. Excluded are the war excess profits tax (1917), victory tax (1942-1943), Social Security self-employment tax (starting with 1951), tax under the income averaging provisions (1964-1986) and under the farm income averaging provisions (starting with 1998), and the recapture taxes resulting from having to recompute and pay back certain tax credits in later years (starting with 1963), the maximum tax on earned income or on personal service income (1971-1981), the minimum tax on tax preferences (1970-1983), and the alternative minimum tax on tax preferences (starting with 1979).

Also excluded are such other taxes as the tax on recipients of accumulation distributions of trusts (starting with 1954) and the special averaging tax or multiple recipient special averaging tax on recipients of lump-sum distributions from qualified retirement plans (starting with 1974). In addition, data excludes the taxes associated with the preferential treatment of capital gains, starting with 1922 (although certain gains received preferential treatment as early as 1918). At various times, these treatments have taken the form of special tax rates; special definitions; different asset holding periods; ceilings on taxes; and exclusions from income. Included among these special treatments were alternative tax (1938-1986) and its variations for the earlier years, although all of these taxes were in some way tied to a structure for regular tax.

Until 1948, a single set of tax rates applied to all taxpayers, regardless of marital or filing status, and married couples filing joint returns were taxed on the combined income of each spouse. However, a second, lower set of rates was introduced, starting with 1948, for married couples filing jointly. To simplify the data presentation for these more recent years, only the lowest and highest tax rates for married persons filing jointly are shown. Under this change, the combined tax of husband and wife became twice the combined tax that would have applied if their combined taxable income (net income for years before 1954) were cut in half. Thus, taxpayers using the joint return filing status split their incomes for tax purposes, in effect doubling the width of their taxable income (or net income) size brackets. The lowest and highest tax rate brackets are, therefore, the brackets for married couples filing jointly that result from taking into account this doubling of the bracket widths. Starting with 1952, a third set of rates was introduced (not shown) for heads of household, i.e., for unmarried individuals who paid over half the cost of maintaining a home for a qualifying person (e.g., a child or parent), or for certain married individuals who had lived apart from their spouses for the last 6 months of the tax year. This filing status was liberalized, starting with 1970, and provides approximately half the advantage of the income-splitting described above. Starting with 1954, the full benefits of income-splitting allowed married couples filing jointly (i.e., the same tax rates and taxable income brackets) were extended to a new, fourth filing status, surviving spouse (i.e., individuals widowed for 1 to 2 years following the death of a spouse, provided they had a dependent child and had not remarried). The remaining filing status was for single persons, who used the rates formerly applicable to taxpayers in general. However, these latter rates were moderated, starting with 1969, by limiting the tax so that it would not exceed 20 percent more than the tax on married couples filing jointly. One result of the 1969 law change was that certain married couples filing jointly had to pay more tax than they would have paid if each spouse had filed separately. To help mitigate this effect, a special deduction in computing adjusted gross income was allowed for 1982-1986 for two-earner couples filing jointly. This deduction was initially 5 percent of the lesser of $30,000 or the earned income of the spouse with the lesser earnings. The percentage was increased to 10 percent, starting with 1983. The deduction provision was repealed, starting with 1987, when new, lower rates and a reduced number of tax brackets began.

For tax years preceding 1954, the lowest tax rate was either the rate for the basic normal tax (if there was just one rate for normal tax) or the lowest of the several rates for normal tax (if there was more than one rate for normal tax).

The highest tax rate was the sum of the uppermost of the graduated rates (if any) for normal tax, plus the uppermost of the additional, graduated surtax rates, provided that both rates were applied to the same income. For example, for 1932, there were two graduated rates for normal tax, 4 percent (on the first $4,000 of income) and 8 percent (on all income over $4,000), and graduated rates for surtax that ranged from 1 percent to 55 percent. The lowest rate for 1932 is, therefore, shown as 4 percent (the lower of the two normal tax rates) and the highest rate as 63 percent (the sum of the 8-percent higher, graduated rate for normal tax on income over $4,000, plus 55 percent, the highest of the graduated, surtax rates, on income over $1 million.). As another example, for 1941, there was just one rate for normal tax, 4 percent, but it applied to all income. The lowest of the surtax rates, 6 percent, was applied to all income under $2,000, so that income under $2,000 was taxed at both the 4-percent normal tax rate and the 6-percent surtax rate. Therefore, the lowest rate for 1941 is 10 percent, the sum of these two tax rates. The highest rate is the sum of the 4-percent normal tax on total statutory net income, plus the highest graduated surtax rate, 77 percent on income over $5 million, so that income over $5 million was taxed at 81.0 percent, the sum of the two rates.

For tax years starting with 1954, normal tax and surtax rates were, in effect, combined into a single rate structure.

For more information on the specific adjustments, see Appendix to Selected Historical and Other Data Tables at https://www.irs.gov/uac/soi-tax-stats-historical-table-23

Suggested Citation:

U.S. Department of the Treasury. Internal Revenue Service, U.S Individual Income Tax: Tax Rates for Regular Tax: Lowest Bracket [IITTRLB], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/IITTRLB, .

Related Data and Content

Data Suggestions Based On Your Search

Content Suggestions